And Yet It Falls?

A Rundown on "The Law of the Tendency of the Rate of Profit to Fall"

This essay was written a few months ago for the end of my sophomore year of college. As such it has the marks of an academic economics essay, but I felt like posting it to add to my mixed “portfolio”. Addtionally this is my first thorough engagement with this debate in Marxist economics. I am not at a level where I can fully understand all the math in the various arguments which I engaged with. Additionally there are some important perspectives I do not touch on, most importantly, to me, is Anwar Shaikhs. I simply did not have a strong enough grasp of his argument in order to give it a fair placement. I am also unsure still whether my presentation of the econophysics perspective is accurate. Either way, I am very open to and hopeful for constructive criticism.

Introduction

The generative code of capital dominates the multiplicities of social life, its logic reduces all things to a function in the circuit of monetary accumulation. From various outlooks of this social life, there stands out a severe contradiction between capitalism and many human interests. There is, however, another way to critique capitalism. What if the very logic of capitalism undermines itself? One of the long standing arguments used to justify capitalism is the dynamistic increases in productivity that it has brought about, and all the opportunities this has afforded us. What if this exact process is itself the achilles heel of capital? This is what lead Marx to triumphantly declare that with development of capitalisms contradictions:

“Capitalist production constantly strives to overcome these barriers, but it overcomes them only by means that set up the barriers afresh and on a more powerful scale. The true barrier to capitalist production is capital itself. “

This quote follows from Marx’s exposition of the “Law of the Tendency of the Rate of Profit to Fall '' (LTRPF) in Capital, Vol. III. It was in this that Marx believed to have found capitalism's internal route to self-destruction. Now, this was not an original theory of Marx’s, and can be found in the classical political economists Adam Smith and David Riccardo. These two highly influential figures had different explanations for what they saw as a simple empirical fact. It was Marx who saw the falling rate of profit as part of the basic laws of capitalist accumulation over time. As capitalism accumulates, and as it develops the productive forces, the rate of profit falls, causing oscillations and crises within the system, threatening the viability and legitimacy of its own existence. Destroying itself as it piles up the misery of the working class. Over time capitalists would have to put in more and more to get the same amount back, starting business becomes harder, riskier. The allure of speculation and other forms of fictitious capital grows stronger, leading to crises and contractions in accumulation. One can even imagine the profit rate being pushed to its limit, hovering just around 0%, the absolute breakdown of the capitalist system.

If this is true, it would be a damning internal critique of the viability of Capitalism. Keynsian and other reformist policies would appear at the very least weaker. If the profit rates are falling, no amount of direct spending or directed credit will save it in the end. However, for decades after the publishing of Capital, Vol. III posthumously in 1884, there was little to no mention or use of this theory. You will not find it very present in the work of Hilferding, Luxembourg, or Lenin. Up until the 1970s only two economic thinkers of note were promoting this theory as important to Marx’s critique of capitalism: Henryk Grossman and Paul Mattick. For example, in Paul Sweezy’s classic 1942 textbook on Marxian Economics, The Theory of Capitalist Development, “the law” took up nothing more than a few, critical, pages. Later in the 60’s and 80’s, with economists Nobuo Okishio and John Roemer, it became widely regarded that the law had been totally refuted.

It was not until Anwar Shaikh, Fred Moseley, and Robert Brenner in the 80s and 90s presented arguments and empirical data in support of the theory, that it regained serious relevancy among the academic Marxist crowd. This resurgence, however, was still secluded to the realm of academia. It was only with the shock of the 2008 financial crisis, that this really began to catch general attention. Those who held up “the law” made their move to claim that they had the explanation for the global meltdown. This move found its first full exposition in the 2011 book The Failure of Capitalist Production by Andrew Kliman. Since then, a series of Marxist economists, most notably Michael Roberts, have published a vast array of essays defending the theory of the law. Countless studies have come out purporting to demonstrate that the rate of profit has in fact fallen over time. One volume which combines much of this is the 2022 work World in Crisis: A Global Analysis of Marx's Law of Profitability, edited by Michael Roberts and Guglielmo Carchedi.

An example of a study showing a falling rate of profit.

Source: Basu, et al (2020)

The theory and the evidence regarding the movement of the rate of profit have serious implications. As stated above it can have a large impact on the effectiveness of economic policies. Across the globe the differential of profitability between nations sets the stage and conditions for the movement of capital, and the dynamics of imperialism. Today we see an increasing re-globalization as industries move to locations with lower wages, greater room for technological development, and more advantageous supply routes. A falling rate of profit may suggest an increasing level of difficulty in recovering from crisis and long-term stagnation. More speculatively, it could put pressure on those among the ruling class to find a logic, other than capitalism, to reproduce their reign.

There are, however, still many Marxian academics who do not believe there is a tendency for the rate of profit to fall over time. Some dispute the appearance of evidence, claiming improper methods of statistical analysis and unclear meanings of the data. Others continue to maintain that the Okishio theorem proved that there could never be a tendency of falling profit rates from increasing productivity. More recent figures, such as the influential Marxologist Michael Heinrich, have argued that Marx’s formulation of the law is, itself, indeterminate. Heinrich even claims that Marx appears to have abandoned it himself later in life. Even some of those who defend the law in its original formulation, such as Andrew Kliman, hold that it is an explanation of a fact, rather than a prediction of what must happen.

The concern of this paper is primarily about whether or not there is a tendency of the rate of profit to fall over time within the logic of capitalism itself, from a Marxist lens. It is less concerned with the debate around the empirical studies, although this will necessarily have to be considered. Beginning with Marx, these arguments have principally been waged around the question of technical change. His argument rested on the idea that productivity-increasing technical change under capitalism would necessarily lead to a long term fall in the rate of profit. On the other hand, the critics of Marx have argued that technical change may lead in the opposite direction. With no discernable macroeconomic law for how technical change must occur, these debates end up being concerned with the microeconomics of firms' choices and diffusion of technology. The result appears to be totally indiscernible chaos.

There is, however, another way to look at the matter. Rather than trying to formulate a deterministic law of how technical change must occur over time, we can look at the context in which it exists. Particularly the context of the average rate of profit on a macro scale. While the rate of profits in real economies are all over the place, when we talk about the fall in the rate of profit over time, we are talking about the average. There are countless factors into how this rate of profit will move over time, and its movement may appear quite random. However we can see these movements exist within constraints, their probability distribution being subject to a kind of law. This style of approach is known as “econophysics” or “probabilistic political economy,” pioneered in its contemporary form in the 1983 work Laws of Chaos.

We can look at what the rate of profit means, what it expresses. It is the formal monetary representation of the accumulation of value. The rate of profit expresses the limit, or the constraint on the growth of capital. Accumulation of capital is what the Marxian critique of capitalism ought to be focused on, as it expresses the actual power of the capitalist class. If we are to begin with the Marxian axiom that living labor is the ultimate source of non-inflationary monetary growth (measured in prices), then its dynamics are also the basic limits of the profit rate. This paper will defend the argument that the macro dynamics of the employed population largely determine the long-term tendency in the rate of profit, and set the conditions within which technical change affects the rate of profit.

Marx’s Formulation of the Law in Capital Volume III

In Capital, Volume 3 Marx laid out what he termed “The Law of the Tendency of the Rate of Profit to Fall.” In Marx’s eyes, this was nothing other than “the expression, peculiar to the capitalist mode of production, of the progressive development of the social productivity of labor.” As the productivity of labor increased over time, and as capital accumulated, the rate at which a given amount of money would fetch more money, would fall. While technological progress may be individually advantageous for the individual capitalist in the short term, it is otherwise for the capitalist pack. When that technological progress is generalized, Marx argued, it’s a blow to themselves. Only those with enough capital to keep up the increasingly high outlay costs are left, and the pressure on the economies oscillatory tendencies heats up.

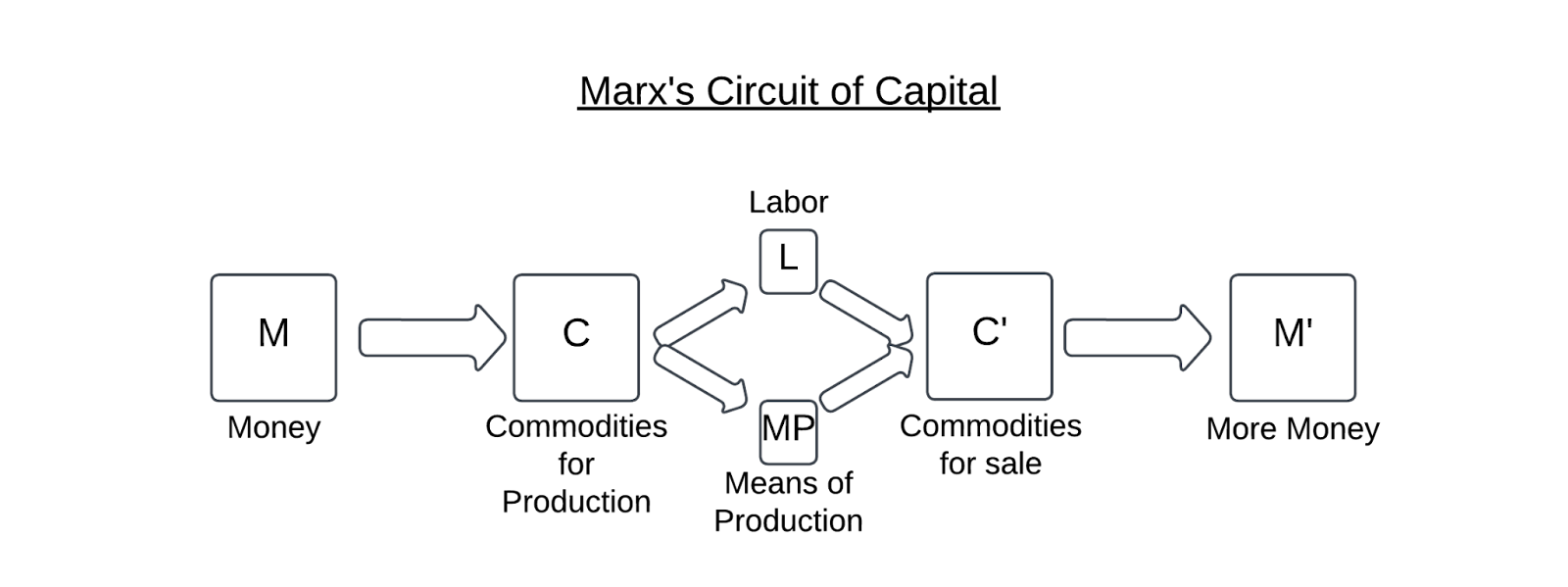

His conclusion, of course, rests on Marx’s fundamental basis. Our human capacity to engage in creative labor, with its ability to be divided in society for social reproduction, is the sole source of economic value. To begin, Marx has some important categories that we need to define. Capital is the movement of money making more money over time ,as an expression of actual economic growth. It can be expressed in the formula M-C-M’, or money -> commodities -> more money. Marx’s circuit can be expanded further to show the breakup of production inputs into labor and means of production.

Marx termed the labor input, its cost in wages, “variable capital”, and the means of production “constant capital.” The extra value, which is the basis for the category of “profit,” is termed “surplus value.” The rate of surplus value is the rate at which x amount of variable capital generates x amount of surplus value, a partitioning of the newly created value. Constant capital does not produce value, but rather merely transfers value. It does this in two ways. In the case of those inputs which form parts of the product, or are used up in their entirety in the production process, their entire value transfers over. These inputs are known as “circulating capital”. For those inputs such as machines, buildings, etc. their value is transferred bit by bit, based on the value divided by the number of production turnovers within their lifetime. These inputs are known as “fixed capital”. It is important for these terms to be clear to understand Marx’s reasoning.

Our discussion of the rate of profit over time will be focused on the rate of profit as it exists at the macro level. What Marx called the “total social capital.” He defined the rate of profit (p’) as the surplus value (s) over the sum of the constant capital (c), and variable capital (v). It is clear that if the rate of surplus value goes up, all other things held equal, the rate of profit will follow. What is equally true is that if the ratio of constant capital to variable capital goes up, all else held equal, the rate of profit will go down. This ratio, insofar as the value ratio expresses the physical ratio, is the “organic composition of capital” (OCC). Marx’s theory of the falling rate of profit relies on his theory about how the OCC changes over time.

On the right equation, we can see how the rate of profit is composed of the rate of surplus value and the OCC. If the OCC rises, then the rate of profit falls. Marx’s argument for the falling rate of profit rests on the claim that the OCC will rise over time, but why would it? Well, this is, for Marx, another way of describing the increasing productivity of capitalist society. A higher productivity means that less time goes into producing the same, or more, products. When new technology is invested in to increase productivity by reducing labor, this changes the ratio of the OCC. If we hold the rate of surplus value constant, this means a falling rate of profit. We can see this using Marxs example in Chapter 13 of Capital, Volume 3:

“The rate of surplus-value is 100%:

If c = 50, and v = 100, then p' = 100/150 = 66⅔%;

c = 100, and v = 100, then p' = 100/200 = 50%;

c = 200, and v = 100, then p' = 100/300 = 33⅓%;

c = 300, and v = 100, then p' = 100/400 = 25%;

c = 400, and v = 100, then p' = 100/500 = 20%.”

While we know that productivity has in fact rapidly increased since the emergence of industrial capitalism, why would any capitalist choose to invest in new technologies, if it will lead to this? Marx’s answer was that, in the short term, it increased their individual profits.

This argument is made in Chapter 15 Capital Volume I, when dealing with machinery. We’ll assume there is a given cost of wages and an established price on the market for whatever product is being produced. When the capitalist invests in new machinery, such that the new outlay on machinery is less than the cost of the labor the capitalist saves, overall costs fall. Now the capitalist is producing the products quicker and cheaper. She can get a competitive edge by selling the product for the same price, or even a little bit cheaper, and makes what Marx termed “super profits”. This is because the labor time required for production in her firm is less than the socially average.

Things become different when this technology is generalized across the industry. Now the socially average labor time goes down, and so the standard price of the commodity goes down. Those super profits disappear. For those companies that were able to transition quicker, their expansion due to these super profits allow them to make more profits than before, even with a lower rate. Those less fortunate companies, who were unable to make the transition, may falter and get eaten up. In Capital, Volume I this is explained in the context of the section on “relative surplus value”. There are two ways to increase the rate of surplus value for Marx, absolute and relative. Absolute surplus value is an absolute increase in the amount of value produced, either through an extension in the working day, or intensification of work. Relative surplus value is an increase in the rate of surplus value through decreasing the value of wage goods, by increasing productivity.

If we hold the organic composition of capital constant, then clearly relative surplus value increases the rate of profit. Marx is actually arguing that the same process that causes this increase, ultimately causes the rate of profit to fall.

“The law of the falling rate of profit, as expressing the same or even a rising rate of surplus value, means in other words: taking any particular quantity of average social capital, e.g. a capital of 100, an ever lesser portion of living labor.” (pg.322)

What Marx is assuming here is that, as the course of increasing productivity goes on, the rate of the rising OCC will be dominant over any rise in the rate of surplus value. It is not totally clear why Marx believed this, and Marx does not offer a full argument to this point. Perhaps Marx was basing this on the analysis he laid out in Chapter 3 of Capital, Volume III on the rate of profit and rate of surplus value. In this chapter Marx shows how the rate of profit is more sensitive to the OCC, concluding that the OCC is more determinate of the rate. Additionally, Marx, in Chapter 15 of the same volume, provides an example in which the wages are pushed down to their limit. Here relative surplus value has exhausted itself. In this context the OCC can still rise, and does not seem to have a hard limit, leading to a fall in the rate of profit. There is the other matter that during Marx’s time it was considered a generally accepted fact that the rate of profit does fall, with varying economists attempting to explain its cause. We will touch on all this later, when dealing with Heinrich.

This being said, let's assume Marx's position, and continue on. Marx does not argue that the rate of profit will simply fall in a straight line down, but rather tendentially, interspersed with times of a rising rate of profit.

“Counteracting influences must be at work, checking and canceling the effect of the general law and giving it simply the character of a tendency, which is why we have described the fall in the general rate of profit as a tendential fall.”

Marx layed out 5 core counter-influences to the falling rate of profit: 1) The increase in surplus value outside employment of technology, e.g. changes in management, longer working day, more intense labor. 2) Reduction of wages below their value via increased domination of the working class. 3) Cheapening of constant capital, such that use of new technology does not increase the OCC. 4) Increased employment in those industries which are, by their nature, labor-intensive, such as luxury artisan goods, especially those with higher rates of surplus value. 5) Foreign trade-relations, either through the purchasing of cheaper constant capital, exploiting different levels of productivity, or from the investment of capital into countries with more labor-intensive techniques of production.

In Marx's view, none of these could outweigh the tendency of the rate of profit to fall. All of them either have their limits, being outstripped by greater capital-intensity, or themselves lead to a rising OCC. This theory, the law of the falling rate of profit, presented itself as the capstone of Marx’s analysis of the core functionings of capitalism: The general law of capitalist accumulation. In Capital, Vol. I, Marx characterized the general law of capitalist production to be that the constant accumulation of capital is mirrored by the increased exploitation & disempowerment of the working class. As time goes on, it would lead to the opposite of free competition and bourgeois progress: despotic monopolies and unemployed criminals. In Capital, Vol II he derives that the reproduction of this development must happen in a chaotic and unbalanced manner, constantly threatening crises. Finally with Capital, Vol III, Marx comes to the damning conclusion that this same law of perpetual accumulation turns against itself and threatens the expansion of profit itself, on its own grounds.

The Critiques of Indeterminacy and Rational Choice of Technique

Michael Heinrich, a prominent scholar of Marx, has argued for many years that Marx failed to formulate a working law of the falling rate of profit. Pulling from mostly unknown writings, he also argues that Marx himself seemed to abandon the “law” in the later years of his life. This is most comprehensively argued, for english readers, in his Monthly Review article “Crisis Theory, the Law of the Tendency of the Profit Rate to Fall, and Marx’s Studies in the 1870s” from 2013. It is this work which we will be directly referencing. Heinrich claims that if we want to treat Marx's analysis of the rate of profit seriously, we must begin with his framework. This framework, for Heinrich, is to look at capitalism in its “ideal average”, to unveil the typical movements of capital, outside any impurities.

“Accordingly, with regard to his arguments for the law of the rate of profit, Marx does not assume any particular form of market or conditions of competition, but rather solely the form of development of the forces of production typical of capitalism, the increasing deployment of machinery. If the law he derives at this level of abstraction is correct, then it must be valid for all developed capitalist economies.”

Marx must then demonstrate that if there is a law of motion in which the rate of profit must fall over time, this has to work for the general movement of capital, in any form of capitalism. Heinrich contends that Marx failed to do so. Firstly, however, Heinrich looks at Marx as a critic and student of the old political economists. Both Adam Smith and Ricardo had theories of a falling rate of profit. Smith's argument was that fierce competition between capitalists would push prices down, and hence profits would fall. However, if we generalize this to all capitalists, both Ricardo and Marx argued, then input goods would also be subjected to falling prices, causing rising profits. Ricardo went for a more dynamic explanation. In his observations of agricultural trends, Ricardo saw that worse and worse land would have to be cultivated. This would require more effort to get the same product, increasing the price of grain, forcing wages up and profits down. Marx disagreed, arguing that with development of productivity in industry, agricultural productivity would develop, even for worse land.

We can then see part of Marx’s work as explaining why the rate of profit can fall down, on its own basis, with increasing development of productivity. Heinrich finds this to be a development over Smith and Ricardo, but that Marx does not move beyond this. Let us look at Heinrichs precise critique of Marx’s LTRPF. If we recall, the rate of profit is determined by two ratios, the rate of surplus value, and the organic composition of capital. In Marx’s argument in Chapter 13 of Capital, Volume III titled “The Law Itself”, he initially makes the assumption of holding the rate of surplus value constant. Heinrich argues that the LTRPF cannot really be argued from this position, and that rather:

“The value composition of capital increases because of the production of relative surplus-value, that is to say in the case of an increase in the rate of surplus-value. Contrary to a widespread notion, the increase in the rate of surplus-value as a result of an increase in productivity is not one of the “counteracting factors,” but is rather one of the conditions under which the law as such is supposed to be derived, the increase in c occurring precisely in the course of the production of relative surplus-value, which leads to an increasing rate of surplus-value.”

Assuming a rising rate of surplus value and rising OCC at the same time should be the assumed basis, sticking with the framework outlined above. Heinrich makes the point that when we make this clearly the assumption of the argument, then it comes down to a contention between those two variables. If the rate of surplus value rises faster than the OCC there is a rise in the rate of profit, if the OCC rises faster than the rate of surplus value then there is a fall in the rate of profit. Clearly Marx stands in the latter position, but why? Heinrich claims that there is no proper case made as to why the OCC must always, in the long run, rise at such a greater rate. Hence, the argument appears indeterminate.

We can elucidate this further from a simple numerical example, one that Marx employs in Chapter 15. If we have 24 workers working 4 hours a day, they produce 96 hours of work, half of which goes to wages, giving 48 hours of surplus-labor. Let us then assume that the rate of surplus value rises to the extreme, somehow (one can imagine some sci-fi scenario in which workers survive through a kind of human photosynthesis). The wages are pushed to zero. Let us also assume there has been a massive increase in productivity, such that 2 workers working 12 hours can produce the same number of products as the 24. Now, however, we have only 24 hours of surplus value instead of 48. Marx uses this example as a way to demonstrate the limits of increasing the rate of relative surplus value to counteract the falling rate of profit. This, however, assumes that the amount of capital used to employ the 2 workers is of the same or a higher value. It is here that Heinrich inserts “we cannot exclude the possibility that the capital used to employ the two workers is smaller than that required to employ twenty-four.”

This has implications for Marx’s general argument. When productivity from employing more constant capital increases, it has two opposing effects on the rate of profit. On the one hand the rising OCC has a negative effect on the rate of profit, and on the other hand it can lead to a rising s/v and, hence, rising profit rates. Marx’s argument that the former case will play out seems to have rested on the idea that there was a definite limit to the latter effect. It was the example above that Marx gave to provide this limit. In Heinrichs perspective, without this, the law is left indeterminate, and hence, not a law at all.

While Heinrichs critique comes from a textual analysis of how Marx framed the law, there is much older, more technical critique. In 1961 the Marxist Economist Nobuo Okishio wrote “Technical Changes and the Rate of Profit,” the source of what is called the Okishio Theorem. In the second half of the 20th century this became widely regarded as the definitive critique of the LTRPF. The exposition and expansion done in the 1970’s by the Analytical Marxist John Roemer solidified this influence. Appearing to show that the dominant tendency in capitalism is a rising, rather than falling rate of profit, the Okishio Theorem caused a shift among Marxian economists. Occurring alongside the apparent success of Keynesianism, less focus was put on the supposedly self-destructing contradictions of capitalism. Critiques had to be formulated from different perspectives, leaving revolution increasingly on the wayside.

Before diving into Okishios argument itself, we must lay out some new categories. We can divide the economy into two core sectors: “basic” and “non-basic”. The basic sector deals with the production of direct and indirect capital goods, i.e. means of production and workers wage-goods. The non-basic sector contains the production of luxury goods, or goods that only function as inputs to luxury goods production. A “technique of production” for a given good is defined as: the amount of hours worked, expressed in a set of wage goods at a given wage rate, plus the means of production required. The “real wage rate” is the amount of unit subsistence goods given for a unit of labor time. This is different from the rate of surplus value which would be a unit of labor time for a unit of labor time, (e.g. 2 labor-hours worth of goods for 8 hours of labor). Okishio assumes a constant real wage rate and an equalized rate of profit (as does Marx), which will become more important as the paper goes on.

Okishio begins his criticism of Marx with his derivation of the general rate of profit:

“The proposition that the production techniques in non-basic industries do not influence the general rate of profit was demonstrated by D. Ricardo but denied by K. Marx. The reason Marx could not get the correct result is that Marx calculated the general rate of profit by dividing the aggregate surplus value by the aggregate capital including non basic industries…”

In Okishio’s perspective, the non-basic industries have no effect on the general rate of profit. When the production techniques of those industries change, this does not influence the other production techniques across the economy in establishing a new general rate of profit. This particular criticism does not have the greatest weight on the question at hand. We will, however, alongside Okishio, assume that we are dealing with the basic sector. As such, a change in the technique of production in an industry of the basic sector will affect the general rate of profit. In Marx’s argument the falling rate of profit occurs from the unconscious result of individually profitable acts of different capitalists. Okishio takes up this as his point of entry for his analysis, the choices of capitalists. When we look at Marx’s argument it appears that the profitable acts of the capitalist are the same as those acts which increase productivity. For Okishio, this is an error, as from the capitalist's perspective their interest is simply the reduction of costs. These are not exactly the same.

Generally, we regard increases in labor productivity, insofar as it is not reliant on destructive externalities, as progressive. Marx even referred to this as the “historic role” of capitalism. Being able to produce more in less time expands the realm of freedom against the realm of necessity. However, capitalist incentives do not necessarily always lead to greater productivity. Depending on how the capitalist chooses to decrease their costs, it can go in many different ways. There can be profitable choices that maintain productivity, and there can even be profitable choices that decrease productivity. Particularly we can see the latter case when less productive, pre-capitalist methods of production are employed in the exploitation of very cheap labor. When those choices become increasingly more appealing to capitalists, the relations of production become a drag on the factors of production, and hence, on progressive technical development.

Coming back to Okishio’s analysis of the rate of profit, he argues that because of this incongruency we can make a distinction between two viewpoints: the price rate and the value rate. Interestingly, Okishio derives this idea from the necessity of exploitation under capitalism. When capitalists make a choice to increase profitability, they do so on the basis of the price rate, with a given market price of their respective outputs. We can now go through what would happen from a profitable change in the production technique, based on Okishios argument. Okishio assumes here, for the sake of argument, that this change will also be productivity increasing, in line with Marx. This will require a numerical argument. Let us assume that there is one production good (a), one consumption good (b) ,and that the production good is the output. Let b be equal to $1, and let the established market price of a be $1.78. Let the real wage rate (w) be equal to 2. Then we can set up a given production technique. The production input is 0.8 of a, equal to $1.424. The labor input is 0.1 hours, with a given wage rate of 2, and 2 * $1 = $2, so the consumption good input is $0.1 * 2 = 0.2. The current general rate of profit (r) is 9.61%.

a = 1.78

b = 1

w = 2

r = 0.0961 = 9.61%

(0.8 * a) + (0.1 * (bw)) * (1 + 0.0961) = 1.78

Then we can introduce a technical change. With the employment of 0.05 more constant capital productivity doubles, such that now only 0.05 hours are required, and costs fall. Now the production technique looks like this:

(0.85 * a) + (0.05 * (bw)) * (1 + 0.1036) = 1.78

r’ = 0.1036 = 10.36%

We can see the rate of profit has increased, and how has this happened? Simply because of a reduction in the cost, following the methodology outlined above. In Okishio’s original theorem, when this change generalizes across the economy, the rate of profit is a little bit smaller, but still higher than the initial rate. This is because of his argument that capitalists, making rational choices, will act upon the given price and will have little incentive to lower it. Now, however, the same amount of labor is represented in a greater amount of monetary output. The price rate of profit and the value rate of profit have been driven apart, and as this process iterates, the gap widens. Okishio concludes that Marx’s theory of the LTRPF, when rational choice is considered, does not hold water. Adding that:

“Marx’s failure to get these correct results, in our own view, is due to two causes. The first is his lack of thoroughness in the analysis of the so-called transformation problem. And the second is his neglect of the important character of capitalistic behavior regarding the adoption of new production techniques.”

So far, in our presentation, the result of Okishio’s theorem has rested upon two crucial assumptions. Firstly we will address the divergence between the price and value rates of profit. Allowing this negates the aggregate equality between price and value, which is a basic part of Marx’s system. To break from this is tantamount to breaking from a Marxist economic perspective altogether, and that is not what this paper is addressing. We can, however, alter the assumptions so that this does not occur. Let us go through this same process of technical changes, but with the assumption that the first example sets a definite monetary expression of labor time (MELT), such that 0.1 hour = $.356. Now there will be no price/value divergence.

With the new production technique the equation is now:

(0.85 * a) + (0.05 * (bw)) * (1 + 0.0477) = 1.69

r = 4.77%

The rate of profit has now fallen, as the reduction in labor expended is proportional to the reduction in price. However, we have held the price of the consumption good constant, assuming that the technique has not been generalized. Without going through the complicated dynamics of technique diffusion, we can use a simplified model to see what would happen if it were generalized. In this model, we will assume a one commodity (d) economy, so that the output good is the only input good. In this example we will assume that 1 hour = 1 dollar for simplicity. We will also assume a constant real wage rate of 0.5, and use “L” to represent living labor.

T1: Starting production technique

1d = $1

0.5Lw + 0.5d = 1d

r = 25%

T2: Individual capitalist employs new technique, gaining super-profits at a given price

1d = $1

0.25Lw + 0.6d = 1d

r = 27.5%

T3: Technique is generalized across the economy, such that the MELT is maintained

1d = $.85

0.25Lw + 0.6d = 1d

r = 37.9%

Here we can now see that the rate of profit rising with a productivity increasing change, while maintaining Marx’s assumption that price = value. How did this happen? With the increasing productivity, both the labor cost of the real wage, and the production input go down. Even with the increasing OCC, the increasing rate of surplus value and cheapening of constant capital cause the profit rate to rise. The second assumption, maintained from Okishio’s theorem, is that of a constant real wage rate. With this assumption, any increases in the productivity of wage goods will necessarily lower the wage-cost and increase the rate of surplus value proportionally. These results have been used to argue by many that there can be no fall in the rate of profit over time without a rise in the real wage rate. Since Marx’s original argument is framed in terms of technical change, and not the struggle over the wage, many conclude this to be a refutation of Marx. Some Marxists, however, argue that Marx never held the real wage rate constant, and that its change is a part of the course of technical development. Others have also seen Okishios original argument as demonstrating the failure of Marx’s law of value for understanding capitalism.

The Contemporary Defence of Marx’s Law

The criticisms of the LTRPF endured as the dominant perspective up to the end of the 20th century. This has only been seriously disrupted in the past couple decades. With the renewed interest in Marxist explanations for economic crises following 2008, the LTRPF began to be taken more seriously as a consideration. Among those arguing in favor of the theory's importance, there are a few who stand out. Such figures include Andrew Kliman, Michael Roberts and Guglielmo Carchedi, who all argue that Marx’s original formulation has been correct all along. They have set out to defend Marx against what they see as misinterpretations and breaks with Marx’s methodology.

Considering the large influence of the Okishio theorem, responding to it has taken up a large part of these defenses. In the second chapter of Carchedi’s 2011 book, Behind the Crisis: Marx’s Dialectics of Value and Knowledge, titled “Debates”, he confronts the theorem. Carchedi starts with arguing that its basis is the supposed divergence between cost-reduction and productivity: “Okishio’s cost-criterion states that, if the physical inputs are multiplied by their monetary prices, holding wages constant, lower costs due to increased productivity must increase monetary profits.”

Seizing on the fact that the physical inputs are multiplied by their monetary prices, resulting in monetary output, Carchedi argues that this would require a proportional supply of money. If this were not the case, and there was an increase in the physical rate of profit but the money supply did not increase, then there could not be an increase in the price rate of profit. In Carchedi’s perspective, the proportional increase in money is an unjustified assumption. Additionally, if we stick with Marx, then only an increase in the value output leads to an increase in the mass of money. Any decrease in the value rate of profit would necessarily, then, lead to a decrease in the price rate of profit, even if the physical rate of profit rises. It couldn't be realized with the restricted mass of money. This concludes for Carchedi that the Okishio theorem cannot hold if we adhere to Marx’s law of value. Beyond this, Carchedi argues, Okishio’s method is totally at odds with Marx’s:

“Okishio’s perspective is that of the capitalists, for whom both the labour contained in

the commodities’ inputs and the new labour added are exclusively a cost. Clearly,

if costs are reduced and wages are unchanged, profits must rise. Okishio’s

critique, by seeing labour as a cost (the capitalists’ point of view), disregards

Marx’s absolutely essential assumption that labour is the (only) creator of

value (the labourers’ point of view).”

Already, before Carchedi wrote his defense, Andrew Kliman went after the Okishio Theorem in the 1990’s. Kliman’s goal, as he makes clear in his 1997 paper “The Okishio Theorem: An Obituary” was to refute the theorem on its own basis. This critique centered on the implicit assumption of what happens with prices when technical change is generalized. In Okishios model, the prices stabilize such that the input unit-prices are equal to the output unit-prices. For Kliman, this assumption is why the uniform rate of profit ends up higher than the initial rate of profit in the theorem. He also criticized the theorem’s conclusion for effectively using a physicalist theory of value, rather than a labor theory of value, without making this explicitly clear.

If we consider the change in the rate of profit from the perspective of the total social capital, maintaining a constant MELT, his argument becomes more clear. When the technical change is first introduced, the input unit-prices are higher than the output unit-prices, because the productivity has increased. Then, in the next cycle with the same production technique, the outputs of the first one become the new inputs, and now the input and output prices are equal. In Okishio’s theorem this is the process in which the generalized technical change increases the rate of profit. Kliman agrees that within that assumption, this will hold true. However, Kliman points out, if there is constant technical change the situation is different. With a new technique every cycle, the input prices will always be higher than the output prices, and the rate of profit can fall over time, on the basis of technical change.

Covering other critiques of the law, Roberts and Carchedi published a paper together in 2013 titled “Marx’s law of Profitability: answering old and new misconceptions”. Here they spent the majority of the defense combating the critique of indeterminacy, particularly the perspective of Michael Heinrich as outlined above. Their fundamental critique of Heinrich is that he did not properly frame the argument in terms of the organic composition of capital. Recall that Heinrichs argument rests upon the claim that Marx failed to show that the rate of surplus value has a limited effect on the rate of profit compared with the OCC. These authors contend, instead, that the argument should always be about the OCC. A rising surplus value, they argue, will only raise the rate of profit if the OCC does not also rise enough to cancel it out.

Reconstructing Heinrichs argument with this framing, they claim that what he should have shown was a labor shedding technique that results in the OCC falling. Constructed in this way, they argue that the claim of indeterminateness is actually mistaken:

“However, this indicates indeterminateness only by using an example taken out of Marx’s theoretical context. Marx’s law is framed in terms of tendencies and countertendencies. When new technologies are brought into the production process in order to increase efficiency, as a rule, assets replace labour and the organic composition rises. So the ROP falls. This is the tendency.”

Here they disagree with Heinrichs claim that increasing the rate of surplus value is part of the law in itself. Rather, both relative and absolute surplus value count as countertendencies to the falling rate of profit. In their perspective of Marx’s framing, the point is now to prove that the falling rate of profit is the dominant tendency, and that these other factors are the countertendencies to this trend. Carchedi and Roberts believe that if the law is to be upheld, it must be proven as a predictive statement, as opposed to Kliman, whom they quote saying:

““Heinrich’s claim that Marx failed to prove the LTFRP is rooted in his mistaken belief that the law is an assertion that the rate of profit must, under all circumstances, fall in the long run. In fact, however, the law is not a prediction of what must inevitably happen, but an explanation of what does happen; it explains why the rate of profit does tend to fall in the long run””

And note:

“This argument is unclear. Either the law cannot predict anything - but then it is not much of a law. Or it cannot predict what must inevitably happen but it can predict something that is not inevitable.”

In their effort to demonstrate the logical consistency and predictiveness of the law, they take up a series of different possible movements in technical change. Consider a situation in which there is a simultaneous reduction in the value of labor-power and constant capital, due to an increase in productivity. Clearly this raises the rate of profit, but they argue that this cannot continue and must succumb to a fall. As a rule, they argue, technology changes will be labor shedding. Not only will the value of labor-power fall, but the total new value output per unit of constant capital will also fall. Whether the rate of profit falls or rises comes down to whether the value of the constant capital falls more or less than the shedding of labor. Clearly, here, either one can win out, and the rate of profit may move in various directions. However, Roberts and Carchedi hold that these are merely fluctuations around a dominant tendency. Now, “To show that the ROP tends to fall, we must show that the rise in the ROP must meet an insurmountable barrier.”

Considering the effect of the cheapening of constant capital, we can see this cannot go on indefinitely. At a certain point this will hit a limit, when constant capital reaches a value of 0, at that point this method is no longer an option for increasing the rate of profit. Once this limit is reached they argue that a falling rate of profit will prevail, even with a rising rate of surplus value. Any technological change to increase individual profits would be labor shedding, as per their rule, and hence would lead to a fall in the rate of profit. Even disregarding this rule, with constant capital at 0, the limit of rising the rate of surplus value would necessarily cause a fall in the rate of profit. This forms the “insurmountable barrier” that these authors consider the proof for the falling rate of profit as the dominant, necessary, tendency. Even beyond this, Carchedi, in his book referenced above, argues that without this insight, one falls into bourgeois economics.

“This is the equivalent of orthodox-economics thesis that the economy tends to grow and that this growth is interrupted by periods of crises. This conception has already been addressed above. If one assigns the status of tendency to the downward-trend (from peak to trough), one subscribes to a notion of capitalism as a system tending towards crises, a movement only temporarily interrupted by a contrary movement within the business-cycle. The system lacks an inherent (tendency towards) growth and equilibrium.”

For both Roberts and Carchedi, it is politically imperative for Marxists to adhere to the LTRPF:

“If we cannot predict the inevitability of the tendential fall in rate of profit and thus of crises, we deprive labour’s fight of its objective ground, the recurrent attempt by the system to supersede itself due to its internal contradictions. Labour’s fight, then, rather than being the conscious manifestation of the system’s blind force of self-destruction, becomes a purely voluntaristic act.”

The Evidence, the Problems, and a Macro Reconstruction of the Marxian theory of the Rate of Profit Over Time

Political convictions and logical defenses are not the only reason for the new wave of interest and support for the LTRPF. There is another, strong, pull. Since the global crisis of 1979 there has been an increasing number of empirical studies on the actual trend of the rate of profit, particularly in the United States. The result has been overwhelming evidence showing a downward trend in the average rate of profit for developed countries. Those who have been the greatest defenders of the theory of the LTRPF have also been at the forefront of this research. As alluded to in Klimans quote above, this evidence demanded an explanation. It spurred the belief that something was wrong about the original arguments against the theory. Beginning, here, it is worth going over some of the empirical research, and also its problems.

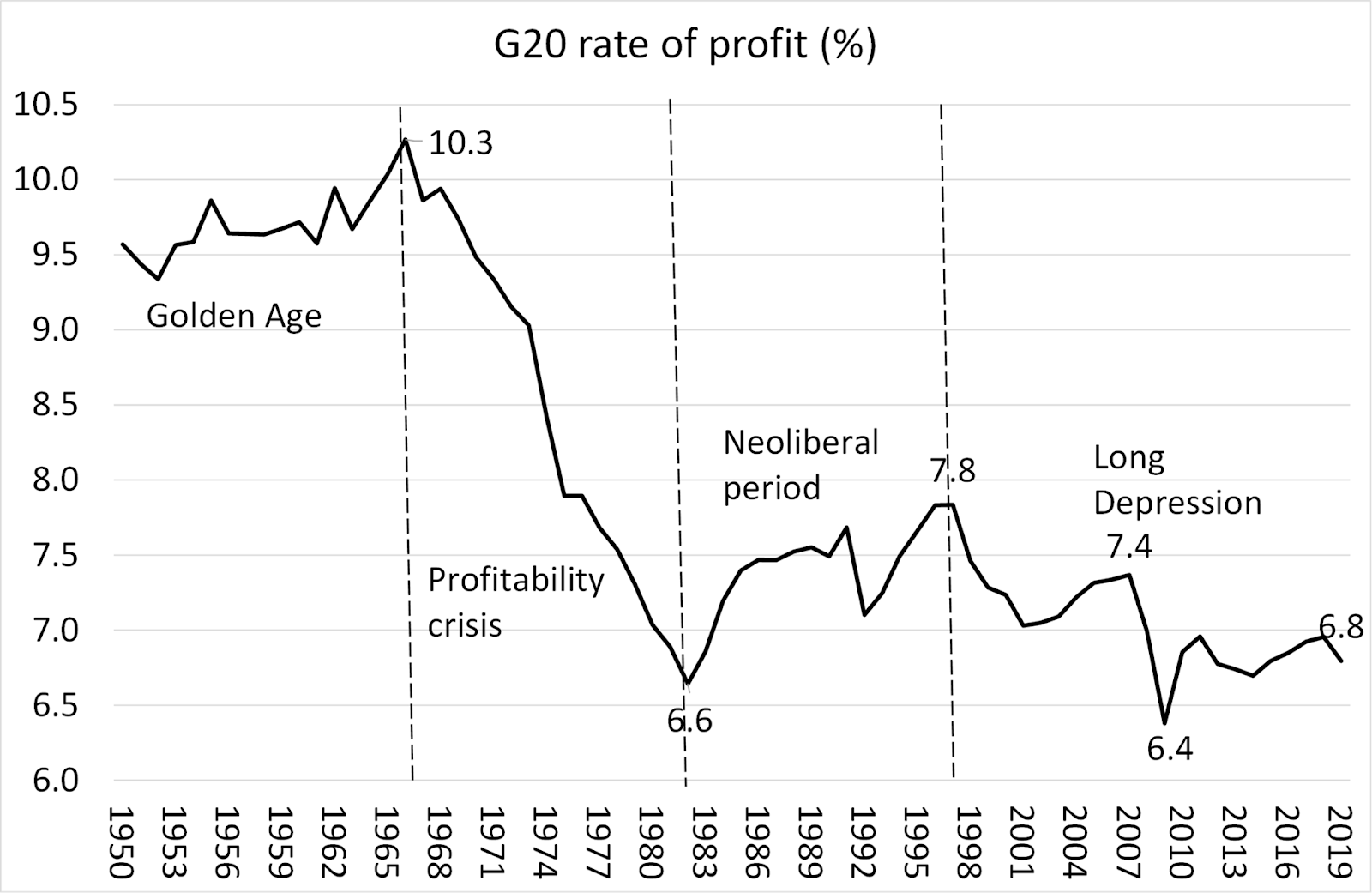

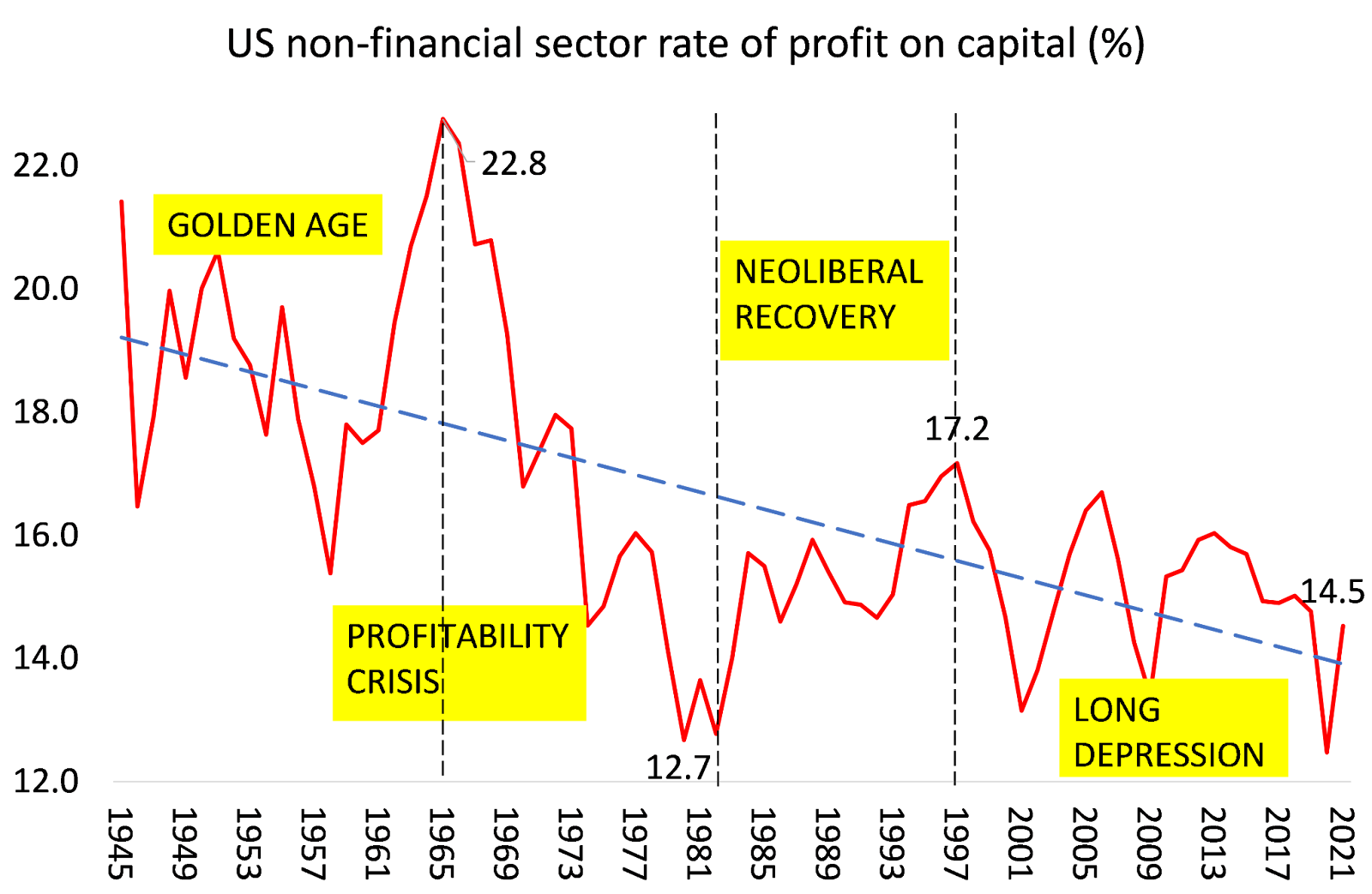

Source: Michael Roberts (2021)

Michael Roberts made this graph using a fairly standard method, among Marxists, of measuring the rate of profit using available economic data. Without going too detailed into the rationale and problems with using available categories of data to extrapolate a Marxian rate of profit, there are some important points to cover. Across the different methods of measuring, all of the studies of the US have produced basically the same graph. Particularly they all agree with the pattern of a severe fall in the late 60’s and 70’s, a recovery during the 80’s and 90s’, and a relative fall into the 21st century. Many Marxists have exclaimed this as a definitive empirical proof of Marx’s law. The truth is, however, not so simple.

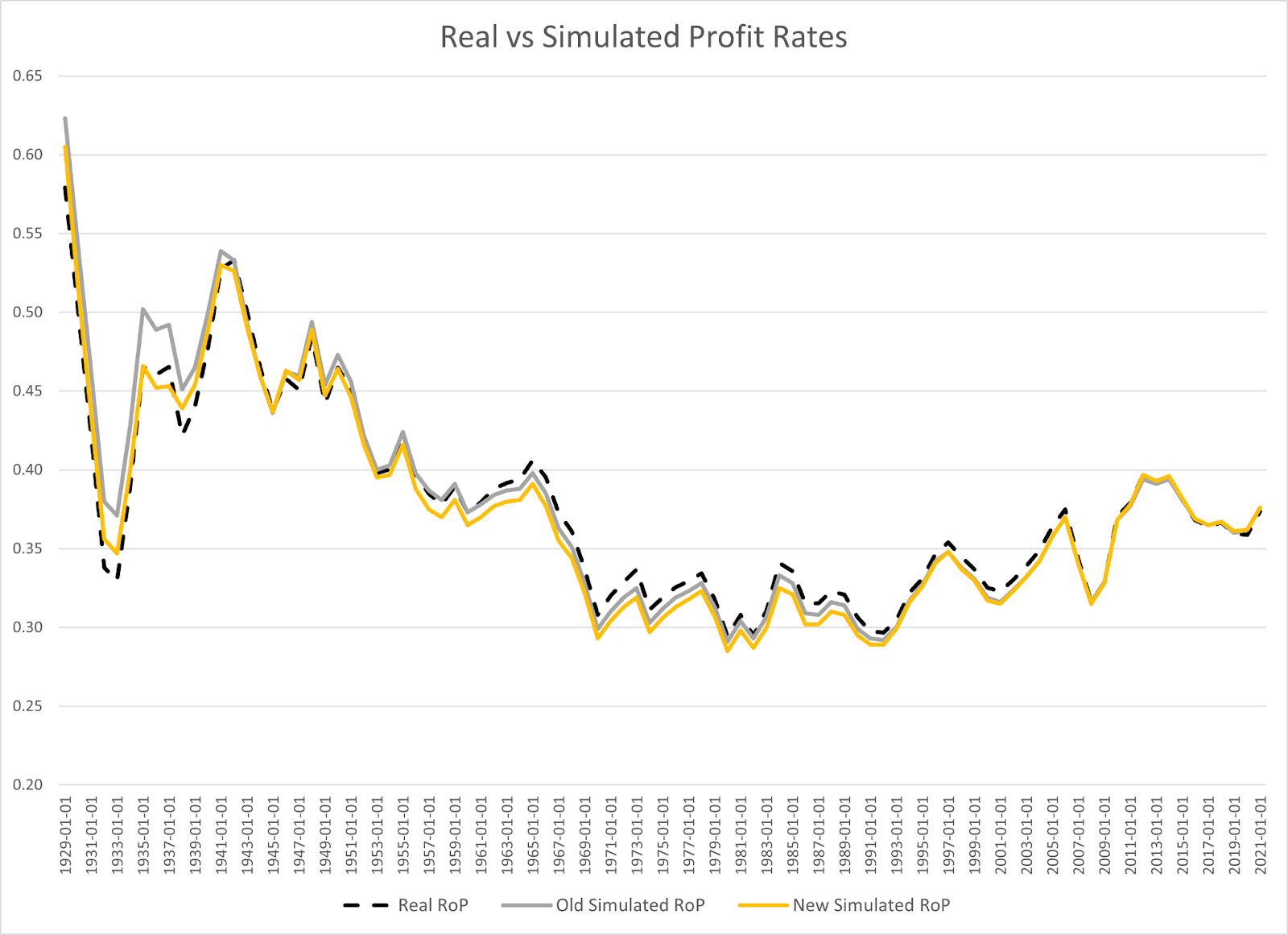

What does it actually mean to empirically prove Marx’s law? It would mean not only showing that the rate of profit has fallen, but also that it has fallen precisely due to the reasons the law said it would. Whether this has been successfully established is now a topic of increasing debate, as the immediate awe of spectacular graphs has subsided. All of the discussions we have considered so far have dealt with the theoretical question of whether the law should play out. Only a very small amount of attention among those involved has been put on whether the, very real, fall in the rate of profit has actually occurred due to a rising organic composition of capital. It should also go without saying that a simple correlation between the two is not enough to this end, such as that shown in the first graph below. There has, though, been some better, more promising work done in this respect. A computer simulation, using Marxs law, made by the independent academic Nico Villareal seems to predict the real fall in the rate of profit, as we see in the second graph below.

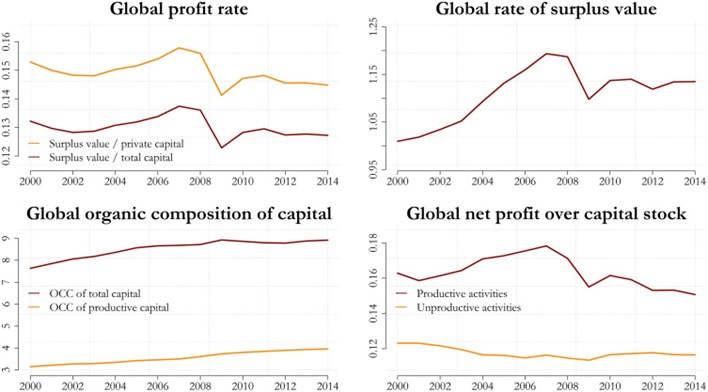

Source: Rutta & Kumar 2024

Source: Nico Villareal 2022 (https://nicolasdvillarreal.substack.com/p/on-the-determination-of-profit)

It is quite understandable that people look at these graphs and see a triumphant repudiation of Marxs critics, and proof that the old master was right all along. This is especially true if it is combined with the political motivation of those such as Roberts and Carchedi. However, until there is more complete evidence that takes into consideration the effects of different variables, it is not such a triumphant moment. That being said, the data so far has leaned in favor of the position that the rising OCC over time has at least partially caused the downward trend. Existing analyses which take into account multiple variables also show how other factors, such as rising real wage rates, lead to this fall. “Is There a Tendency for the Rate of Profit to Fall? Econometric Evidence for the U.S. Economy, 1948-2007” by Basu and Manolakos published in 2010, is one of the best studies to this end, so far. This study explicitly takes into account the countertendencies that Marx outlines, breaking down the short-term, medium-term, and long-term causes of the falling rate of profit over time. More studies ought to be made with a similar level of rigor.

Continuing along in this paper, we will assume that the evidence showing a falling rate of profit is correct, and that it is at least partially caused, in the long run, by a rising OCC. We now have to consider how this empirical backdrop relates with the theoretical debates outlined above. Let us first take a closer look at the debates that we addressed. It appears that the arguments in favor of the LTRPF as logical prediction of what must happen consisted of two: that there are absolute limits on raising the rate of profit through technical change, and that only new living labor engenders new money. It should be immediately stated that the latter argument is completely alien to Marx and the majority of political economists. What Marx directly argued was that prices, divided by the velocity of money, determine the money supply. This is not the same as saying that new value determines the money supply. Actually, from Carchedi's own framework, one could derive that if not enough new money was created, then labor would not create new value. To be more fair to the argument, it is getting at what was more coherently done in the 1980’s by Duncan Foley, in which we take a consistent monetary expression of labor time in prices. This, however, frames the argument as it should be framed: in terms of price, not the money supply.

When considering the question of the limits of raising the rate of profit, we begin to get to the root of the problem with these debates. Roberts and Carchedi argue, in line with Marx, that there are absolute limits on this. This should not be denied. Rather, the problem is whether these limits necessitate that the rate of profit must fall over time. Certainly, once they are hit, the rate of profit can only go down, but these are extreme examples. One could consider a situation in which an economy gets very close to these limits and the profit rates begin to fall. However, there are a multitude of circumstances in which these limits could be loosened, or in which new, shifting, economic development occurs. Maybe one could argue that eventually, after a long time, these limits would be hit for global capitalism. At which point the rate of profit would finally fall, but this is far out of bounds for any argument of relevance.

It seems far more realistic to expect that because the rate of profit can move in various directions, without any necessary tendency, that it will move all over the place. With the evidence in mind, one could say that the fall has occurred due to technical chantes, but this is not a reason to say that it would continue to fall because of this. Here we have basically arrived at the perspective of Heinrich, that the LTRPF is indeterminate. The paper could end here. Marx’s formulation of the rate of profit to fall over time due to technical change is indeterminate. However, there is another way of looking at the perspective, stemming from Marx’s basic axiom that profits come from living labor.

We can already see the embryo for a new perspective within Marx himself. In Capital and elsewhere we see him treating underlying functions and movements as material processes, inter-penetrating each other. Insofar as there are laws in this analysis, they are laws of randomness, like gravitational pulls conditioning the chaotic matrix of relations. What Marx always worked to do was to show how the mess of chaotic, mystical categories of the economy were actually conditioned by a basic sociological necessity:

“Every child knows a nation which ceased to work, I will not say for a year, but even for a few weeks, would perish. Every child knows, too, that the masses of products corresponding to the different needs required different and quantitatively determined masses of the total labor of society. That this necessity of the distribution of social labor in definite proportions cannot possibly be done away with by a particular form of social production but can only change the mode of its appearance , is self-evident. No natural laws can be done away with. What can change in historically different circumstances is only the form in which these laws assert themselves. And the form in which this proportional distribution of labor asserts itself, in the state of society where the interconnection of social labor is manifested in the private exchange of the individual products of labor, is precisely the exchange value of these products” (Marx, Letter to Kugelmann, July 11, 1868)

The various apparent economic categories, price, interest, profit, etc are without a doubt important in themselves, but they are also conditioned by the law of value. Capital, for Marx, is the movement of money for more money, and money is the representation of the command of living and dead wage-labor. In the totality of its relations, capitalism forms a complex web aimed in a direction which it must recorrect towards. Capitalism appears as a cybernetic machine, an artificial intelligence, or even an animistic deity. When we take the inherent chaos of the system, paired with its definite logic as our starting point, we have to address the system differently. We cannot rely on models which take up a deterministic point of entry and then add dynamic fluctuations on top, like a bad patch to broken code.

The movement of the rate of profit is highly complex, appearing almost totally random. Any attempt to derive a tendency by teasing out how different variables act in isolation will always be broken by this chaos. Trying to fix this problem by assuming that the agents involved will act “rationally”, so that a certain outcome can be predicted, does no good. Really, this chaos can only be fully dealt with by the creation of computational dynamic complexity models such as those being developed by Ian Wright, Duncan Foley and Steve Keen. However, at the macro level of the whole economy we can derive some of the most important conditioning factors of this complexity. Much of the argument that will be made in this regard comes from Chapter 13 of the 2009 book Classical Econophysics, titled: “Understanding Profit.”

Let's look at how profit functions in the macro-economy. Firstly, what is it that the rate of profit actually tells us? The rate of potential growth of capital accumulation. Capital is precisely this process. Percentages of profit being reinvested and adding to the growth of capital accumulation, with each cycle. A growth in the command of objectified past labor, and living labor. The money gained from profits only matters for capital insofar as it can be used to acquire more capital, more products and command of actual human activity. We can see that profit, insofar as it is reinvested, is directly conditioned by the underlying factor of real human lives. New growth requires more employees, which ultimately presupposes a growth in the population.

Continuing along this line of thought, we can reframe the basic categories of surplus value, variable capital, and constant capital as the actual people involved in these relations. Surplus value is the number of people whose labor is embodied in the consumption and investment goods whose prices equal the profits. Variable capital is the number of people who are engaged in the production of those consumption goods which are purchased by wages. Constant capital can be reframed as the number of past person-years represented by the capital stock.

We can begin to see how the rate of accumulation is dependent on the access of newly employable workers. If we assume the value wage rate to be constant, the growth of variable capital expresses the growth of new employees. With an increase in wages, i.e. more workers, there is proportionally more profit, and vice versa. The rate of increase or decrease in profit, i.e. the rate of profit, will be determined by the rate of growth of the employed population. We can also see this as determining the year-to-year rate of change of the mass of surplus value. At a given rate of surplus value, and a declining rate of population growth the rate of growth of surplus value will decline over time. With a constant rate of technical change this will express itself as a fall in the rate of profit over time.

Now, of course, the value wage rate does not remain constant, nor the rate of technical change. An increasing rate of surplus value, and rapid cost-reducing technical changes both factor in as counteracting forces. Less necessary labor for wage goods gives more labor to those products which represent profit. With more labor-productive production of the capital stock, the ratio of capital stock to profit decreases. However, in order for these counter-tendencies to win out, they would have to continue every cycle, at a greater rate than the decline in the rate of population growth. Many more complexities could be considered, such as unemployment, central banking, inflation, imperialism, and so on. Some of these are dealt with well in the book referenced above, however, really capturing all these factors would require more developed models.

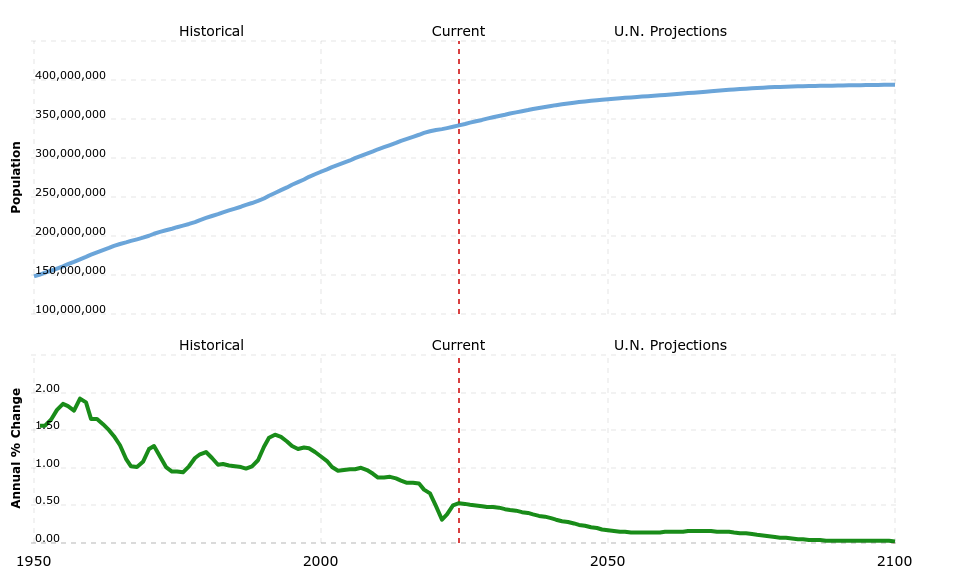

It follows that we cannot make definitive claims, at this level of argumentation, about necessarily how the rate of profit must move. We can say, however, how certain macro factors weigh on the tendency of the rate of profit over time, such as population. If the rate of population growth falls over time, this negatively restricts the rate of profit, and the rate of change of growth itself. If the rate of population growth rises, this has a positive effect on the rate of profit and the rate of growth. How does the rate of population growth move in reality? In industrializing capitalist economies the rate of population growth booms, and in developed capitalist countries it begins to decline and move towards stagnant or declining population sizes

US Population 1950-2024 w/ U.N projections:

Source: United Nations - World Population Prospects

Conclusion and Implications

The movements of the rate of profit over time are incredibly complicated. However, when we understand it as a representation of possible growth, we can see how it is regulated by the growth of the employed population. A falling rate of growth of the population significantly reduces the likelihood that the rate of profit wont fall over time. With a strong degree of confidence we can expect that if the rate of population growth continues to fall, as is expected, so will the rate of profit. Additionally, this pairs with other negative influences such as increasing costs of technology, automation, unproductive labor and rising real wages. With all the recent talk of automating various aspects of retail and production, that begins to become a serious consideration in regards to the rate of profit. It is true, however, that we have definitely deviated from Marx’s original argument, but only by expanding his framework. By the same nature, we should be clear that the argument does assume Marx’s law of value.

We will not deal here with the very interesting and equally complicated problem of how labor time distribution actually expresses itself in capitalist relations, or how this might deviate from Marx’s writings. The debates within that problem have also followed a very similar path as the debates around the rate of profit. It, too, has found a very novel reconstruction within the probabilistic/econophysics school of Marxian economics (see How Labor Powers the Global Economy by Emmanuel D. Farjoun, et al. Published 2022). Moving on, we now have to consider: what are the economic and political implications of a falling rate of profit?

We should first clear away the characterization of the matter by Roberts and Carchedi. Without the LTRPF, there absolutely can be an objective struggle for the emancipation of the proletariat. There are deep contradictions within capitalism that provide not only an objective basis for recurrent crises and the struggle of the proletariat, but also for the possibility of communism. You don't need a teleological necessity that capitalism will slay itself. We can see other important implications of the LTRPF. As the rate of profit falls over time, speculative investments become more alluring, crises more likely, and the capacity for recovery dampens. Stimulus policies lose their effectiveness when they hit the barrier of profitability. Particularly with the recent rise in popularity of post-keynesian politics on the left, this provides another reason for the rejection of reformist policies.

Let's briefly explain how this works. Increasing employment through lowering interest rates and direct spending will lead to a tighter labor market and rising wage rate. The rising wage rate decreases the rate of profit and disincentivizes investments. If the rate of profit falls below the interest rate, this can lead to outright disaccumulation and contraction in production. Falling profit rates in productive investment incentivizes investments in more risky adventures, adding to the rate of inflation. A falling rate of profit over time lowers the profitability barrier at which point these policies become ineffective.

If a government chose to continue with these policies past this barrier, with the same intentions, they would find themselves in direct opposition to the capitalist class. There is also reason to believe that if the capitalist class had to reinvest greater amounts of their profits into production, this would threaten their very existence as a class. Any serious direction of reform in favor of free human development will ultimately find itself in opposition to the capitalist class, and the logic of profit. It would have to break with the structure itself, and maintain its forceful capacity to do so. There would have to be a fight of proletarian, communist interests against capitalist interests. Clearly this would also have to entail an entirely different structure of (revolutionary) government, and a serious internationalism. One of the strongest counter-tendencies to the rate of profit is imperialism and underdevelopment of exploited nations. Unless the global empire is smashed, the core capitalist class may subside the crisis of its own logic, for a while at least.

It is important to also go over what a falling rate of profit also expresses for the other tendencies that exist within capitalism. What if there was an accelerating rate of reinvestment, moving deeper into the logic of technological dynamism for which capitalism is known. As the cycles spurred on the capitalist class would get smaller, eating itself up, and increasingly there would be trouble with finding what to do with the waves of surplus populations. Eventually, profits, as in real surplus value, would go down to 0. Capital could spawn itself anew, existing in a purely fictitious, fetishistic state, as a constant debt to itself with no interest. Capital may even shed the chains of its human birth. With a full development of universal machines, able to replicate the creative capacities of humans and beyond, value would no longer be our monopoly. The rate of growth of the mass of machines producing value could always be higher than the rate of growth of the capital stock. The ruins of human life would be long forgotten by the movement of capital, now terraforming whatever planet-x it came across.

The specific simulation you cite from my blog is showing how the simplified understanding of the Marxist rate of profit matches up to reality by looking at only the rate of exploitation and rate of capitalist consumption/investment to determine the profit rate, rather than worrying about adjustments to the value of the capital stock due to changes in prices/productivity in means of production producing industries. Further down in the blog I show precisely how much is due to rising organic composition of capital vs falling rates of exploitation, specifically that in the US that the organic capital composition grew much slower in neoliberalism. You might find this data on global profit rates going back to the 60s interesting, as while US profit rates stopped falling in neoliberalism, they have continued to fall globally and specifically due to the organic capital composition. https://dbasu.shinyapps.io/World-Profitability/